|

Have you ever envisioned a life where the chains of daily grind are broken well before the conventional retirement age, paving the way for a life of financial freedom and leisure? Embracing financial discipline and frugality can pave the way to a comfortable early retirement, answering the pressing question: Can meticulous financial planning and a frugal lifestyle significantly hasten your journey to early retirement?

Financial planning goes beyond merely saving a portion of your income; it's about understanding and rectifying financial bad habits that may impede your journey towards financial stability. Everyday financial misbehaviors such as impulsive spending, credit card debt, and the lack of a structured financial plan for emergencies often go unnoticed but have a long-term detrimental impact on financial health. Addressing these personal finance habits is the first step in financial planning.

Frugality is about making informed and restrained financial decisions to save money. A frugal lifestyle encourages avoiding unnecessary expenses and finding value in what you spend.

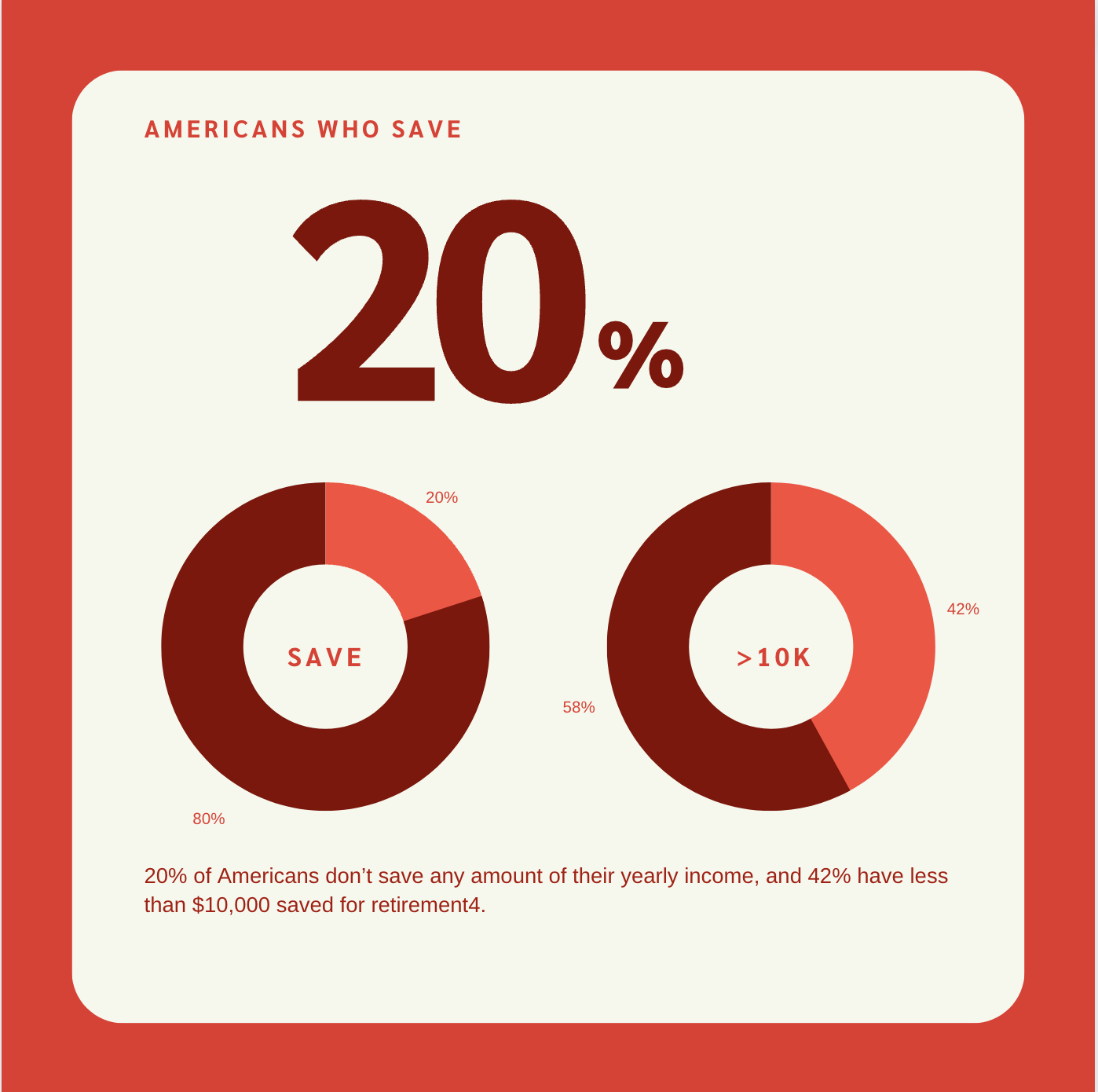

Did you know 20% of Americans don’t save any amount of their yearly income, and 42% have less than $10,000 saved for retirement4.

There are myriad tools and resources available to aid in your financial planning journey. Budgeting apps, financial advisors, and online courses are excellent resources. Trilogy Financial, for instance, offers a Decision Coach program designed to provide additional accountability and coaching to individuals seeking financial guidance.

Easily Meet with a Certified Financial Planner.

The quest for early retirement often begins with a thorough re-evaluation of one's financial plan, identifying areas of improvement, and capitalizing on unforeseen savings opportunities. The year 2020 saw many Americans saving more, with an average of 10% more money saved compared to 2019, mainly due to lifestyle changes induced by the pandemic. Some redirected these savings towards home improvements, while others saw it as a stepping stone towards drafting a solid financial plan aimed at debt reduction, college planning, or accelerating the journey to financial independence.

Various individuals and communities dedicated to frugal living and meticulous financial planning have emerged over the years, showcasing diverse pathways to early retirement. Here are a few noteworthy examples:

These cases highlight the transformative impact of frugal living and prudent financial planning to achieve early retirement dreams. They speak to the importance of continuous financial plan evaluation, adapting to changing circumstances, and leveraging savings opportunities to expedite the journey to financial independence and early retirement.

The road to early retirement is laden with challenges, primarily stemming from our own financial bad habits. However, if we create a financial plan, adopt a frugal lifestyle, and leverage available resources, overcoming these challenges and retiring early is an achievable goal.