The pandemic’s economic disruption altered people’s views on a wide range of money topics—from the feeling of financial insecurity to the extra burden of debt, to how best to protect their loved ones, physically and financially. People’s interest in life insurance—knowing they have a need for it—was heightened during the pandemic and remains so, as people take a closer look at their financial security and well-being. The 2023 Insurance Barometer Study, by Life Happens and LIMRA, shows this trend is prevalent among the younger generations, as well as with single mothers.

Single Moms Need the Industry’s Help

Fewer women own life insurance than men, 49% vs. 55% respectively. And that number is even starker for single moms: Just 2 of 5 single mothers (40%) own life insurance. That said, 6 in 10 single moms (59%) know they have a life insurance need gap—meaning they need coverage or more of it (vs. 41% of all adults) equaling about 5 million households. And 4 in 10 (38%) say they intend to buy coverage this year. With 7.9 million single-mom households, according to the U.S. Census Bureau, there is a dire need for single moms to

purchase life insurance, or more of it.

The primary reason single moms own life insurance (63%) is the same as the general population: to cover burial costs. However, only 26% say they have it to replace lost income. And more than half (51%) say they are “extremely concerned” about leaving dependents in a difficult financial situation if they died prematurely, vs. 29% of the general population.

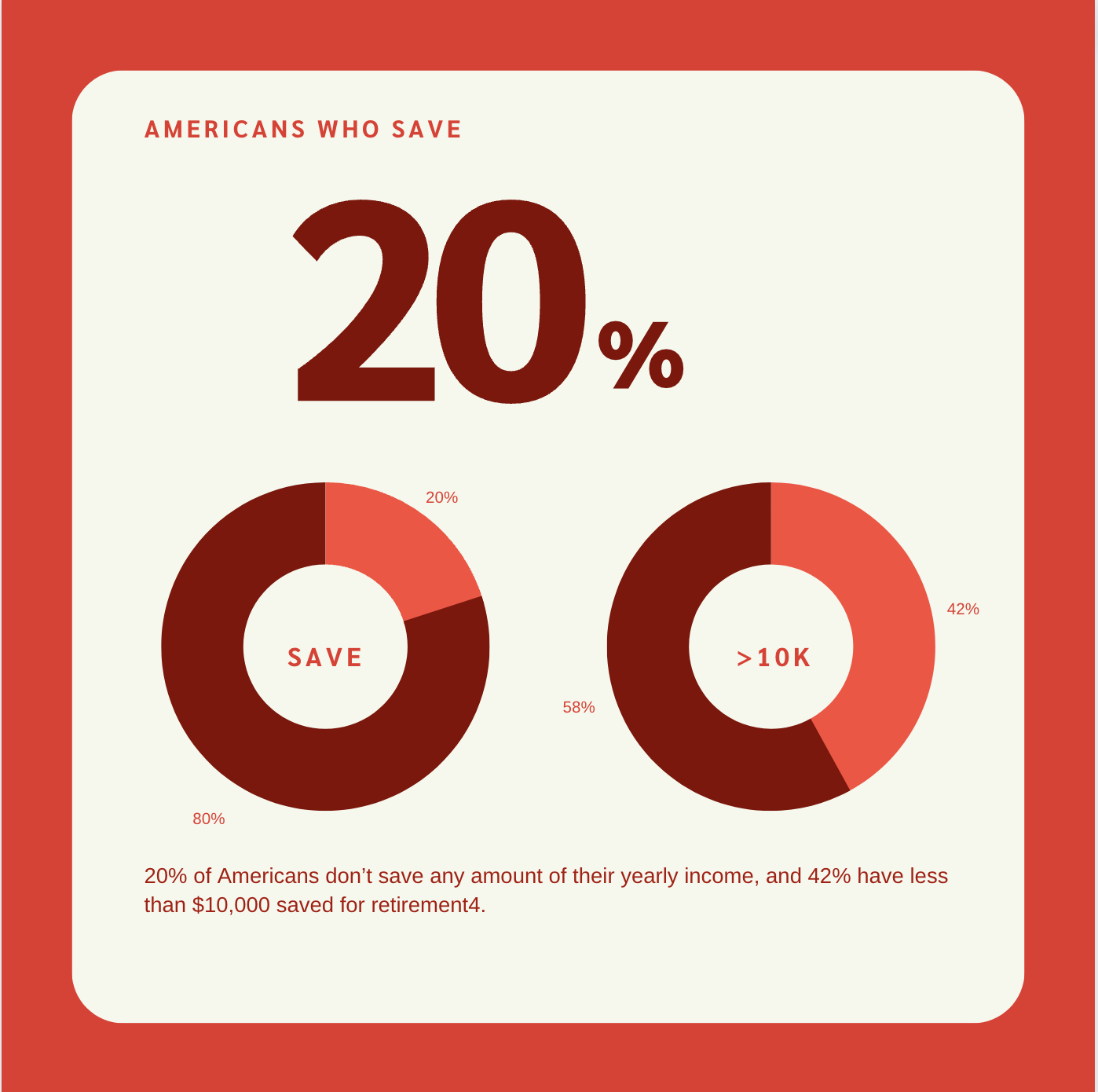

That’s not the only area of financial concern. In fact, single moms have increased levels of concern over a wide range of financial issues—often double-digits—over the general population.

• Having money for a comfortable retirement: 58% vs. 44%

• Saving for an emergency fund: 56% vs. 38%

• Paying monthly bills: 50% vs. 32%

• Ability to afford college: 40% vs. 22%

Owning life insurance makes people feel more financially secure: 69% of life insurance owners feel secure vs. 49% who don’t own. For single moms, this is 52% of owners feel secure vs. 30% who don’t own. The good news is that while only a third of single moms (35%) work with a financial advisor currently, more than half without one are looking for an advisor (52%) to help them navigate their finances.

Desire and Need Are on the Rise

Gen Z is growing up—they’re adults now who are in the weeds of financial responsibilities and stresses. Half of Gen Z is now 18-26 years old, which means 19 million young adults are ready for life insurance, most of whom are non-owners; and Millennials, at 27 to 42, are well into their careers and starting families. The study took a look at life insurance ownership among different age groups and found that half of all adults (52%) own life insurance, with 40% of Gen Z adults and 48% of Millennials currently owning it.

As Gen Z starts hitting life milestones such as finding a partner, buying a home and having children, half (49%) say

they either need to get life insurance or increase their coverage. And Millennials are not far behind, with 47% saying so. And they are ready to take action: 44% of Gen Z adults and 50% of Millennials say they intend to buy life insurance this year.

They also want to purchase it where they have become comfortable—online—and that goes for all generations. In 2011, 64% of people said they preferred to buy life insurance in person; by 2020, just 41% felt this way. In 2023, it dropped to 29%.

Education Is Key for Gen Z

There is work to do on educating people about ownership: 42% of all adults say they’re only somewhat or not at all knowledgeable about life insurance.

A quarter of Gen Z and Millennials say that not knowing how much or what kind of life insurance to buy stops them from getting coverage. And 37% of Gen Z and 27% of Millennials say

they “haven’t gotten around to it.”

Across generations, cost is cited as the top reason for not getting life insurance. But only a quarter (24%) of people correctly estimated the true cost of a policy for a healthy 30- year-old, which is around $200 a year.* More than half of Gen Z adults (55%) and 38% of Millennials thought it would be $1,000 or more.

With the current climate adding financial uncertainties to Gen Z and Millennials, including layoffs and inflation, it is imperative that the two age groups learn how to protect their loved ones financially. Education around finances in general, inclusive of life insurance, will be extremely beneficial, particularly for Millennials, who cite the highest overall level of financial concern (39%).

*Survey respondents were asked how much they thought a $250,000 20-year level term policy would cost per year for a healthy, nonsmoking 30-year-old, which is around $200.

Please source all statistics: 2023 Insurance Barometer Study, Life Happens and LIMRA© Life Happens 2023. All rights reserved.