Introduction:

Selecting a qualified financial planner is crucial for securing a robust financial future. A proficient planner, like those at Trilogy Financial, can create a financial plan tailored to your unique needs to help you reach your goals. Yet, a staggering 74% of Americans engage in financial planning without professional guidance, revealing a potential gap in making informed choices2.

Mistake 1: Overlooking Qualifications

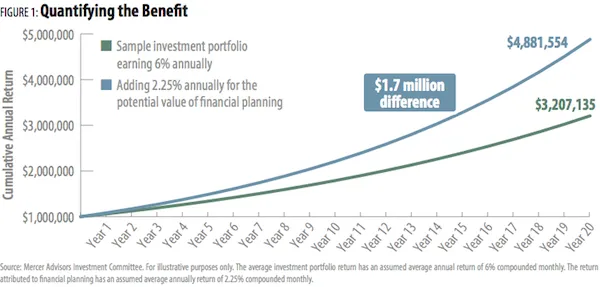

- Stat: Smart financial planning can yield 1.5% more in annual average returns, underlining the importance of qualified guidance3.

- Tip: When choosing an advisor ensure your planner holds pertinent certifications and showcases a robust track record of expertise.

- What are pertinent certifications for a financial planner?Pertinent certifications include the Certified Financial Planner (CFP), Chartered Financial Analyst (CFA), and Certified Public Accountant (CPA) designations. These certifications indicate a high level of expertise and adherence to industry standards.

- How can I verify a financial planner's certifications?You can verify a planner's certifications by checking the databases of certifying bodies like the CFP Board or the CFA Institute. Additionally, you can ask the planner for proof of certification.

- What constitutes a robust track record of expertise?A strong track record includes many years of experience, successful financial planning, happy clients, and industry recognition or awards.

- How can I assess a financial planner’s track record?You can assess a planner’s track record by reviewing client testimonials, checking for any industry awards or recognitions, and asking for references. Additionally, verifying their work history and experience in the field can provide insights into their expertise.

Mistake 2: Neglecting Fee Structures

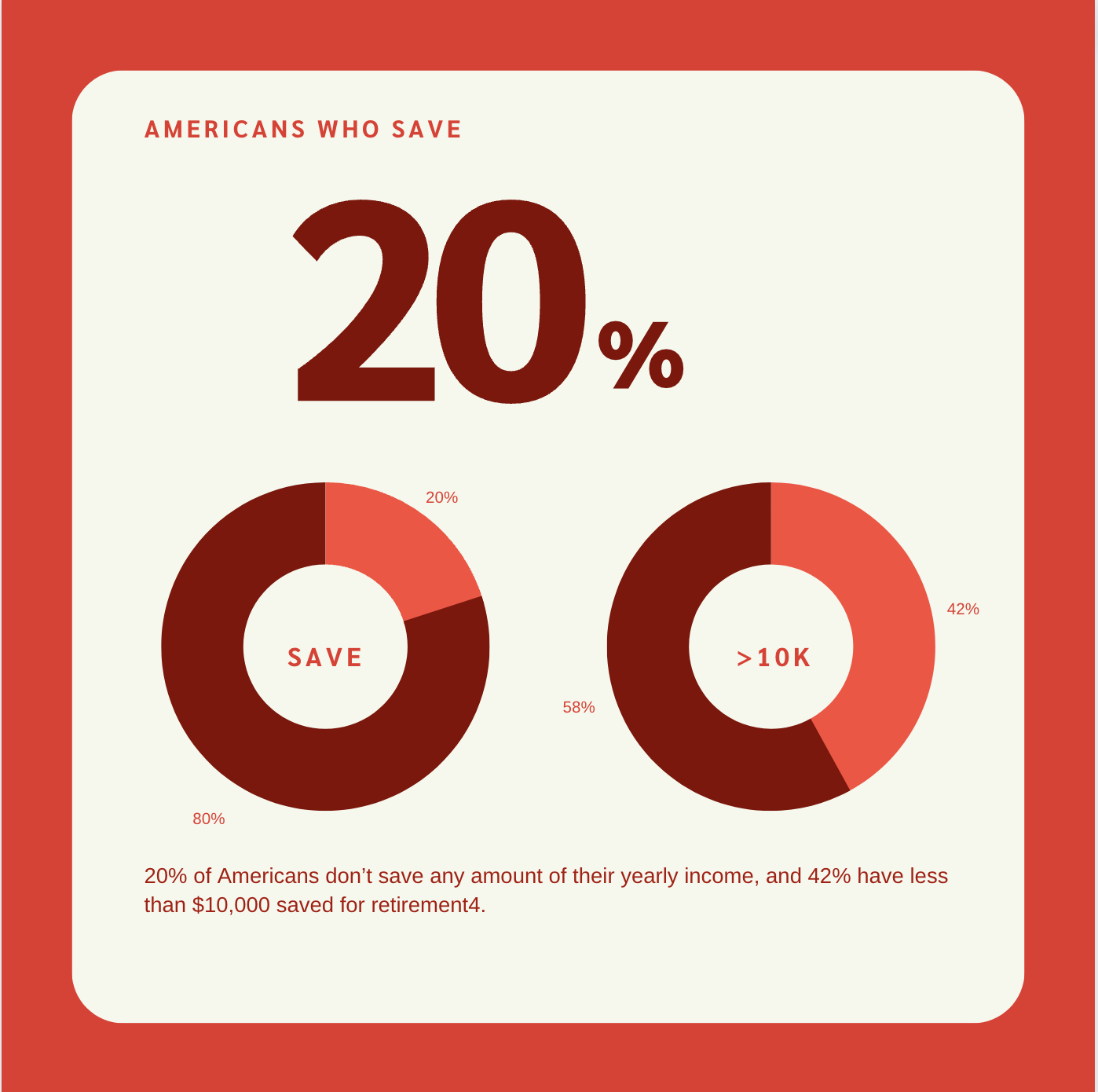

- Stat: According to a 2019 Financial Trust Survey, “Nearly half of Americans (48%) incorrectly believe all financial advisers have a legal obligation to act in clients’ best interests.”4.

- Tip: Understand the fee structures and ensure transparency in your financial engagements if you chose to work with a financial advisor.

- What are common fee structures in financial planning?Common fee structures include fee-only (fixed, hourly, or percentage of assets managed), commission-based, and fee-based (a combination of fees and commissions).

- How can I ensure transparency in fee structures?Ask your financial planner for a clear, written explanation of all fees and charges, including any potential third-party fees, before engaging their services.

- What is the difference between fee-only and fee-based financial planners?Fee-only planners charge a flat fee, hourly rate, or percentage of assets managed, and do not receive commissions from selling financial products. Fee-based planners, on the other hand, may charge fees and also receive commissions, which could potentially lead to conflicts of interest.

- How do commissions affect the advice I receive?Commissions could potentially create a conflict of interest if a financial planner is incentivized to recommend certain products that earn them commissions, rather than what's in your best interest.

Mistake 3: Disregarding a Personalized Approach

- Stat: A Bankrate 2019 survey shows that 44% of individuals with a personal finance plan save more for retirement and 43% save 50% more per month.5

- Tip: When hiring a financial advisor opt for financial planners like those at Trilogy Financial, who prioritize a personalized approach to meet your unique financial objectives.

- What does a personalized approach in financial planning entail?A personalized approach means that the financial planner takes the time to understand your individual financial circumstances, goals, risk tolerance, and future aspirations to craft a strategy tailored to meet your unique needs.

- Why is a personalized approach important in financial planning?A personalized approach ensures that your financial plan is aligned with your goals and circumstances, which can lead to better financial outcomes and satisfaction over time.

- What are some examples of unique financial objectives that would benefit from a personalized approach?Unique financial objectives could include planning for early retirement, saving for a child's education, managing a large inheritance, or preparing for a significant life change like marriage or starting a business.

- How does a personalized approach compare to a one-size-fits-all approach in financial planning?A personalized approach provides tailored advice and strategies based on your individual circumstances, which can lead to more effective financial planning and better outcomes compared to a one-size-fits-all approach that may not align with your personal goals and risk tolerance.

Mistake 4: Ignoring a Comprehensive Service Offering

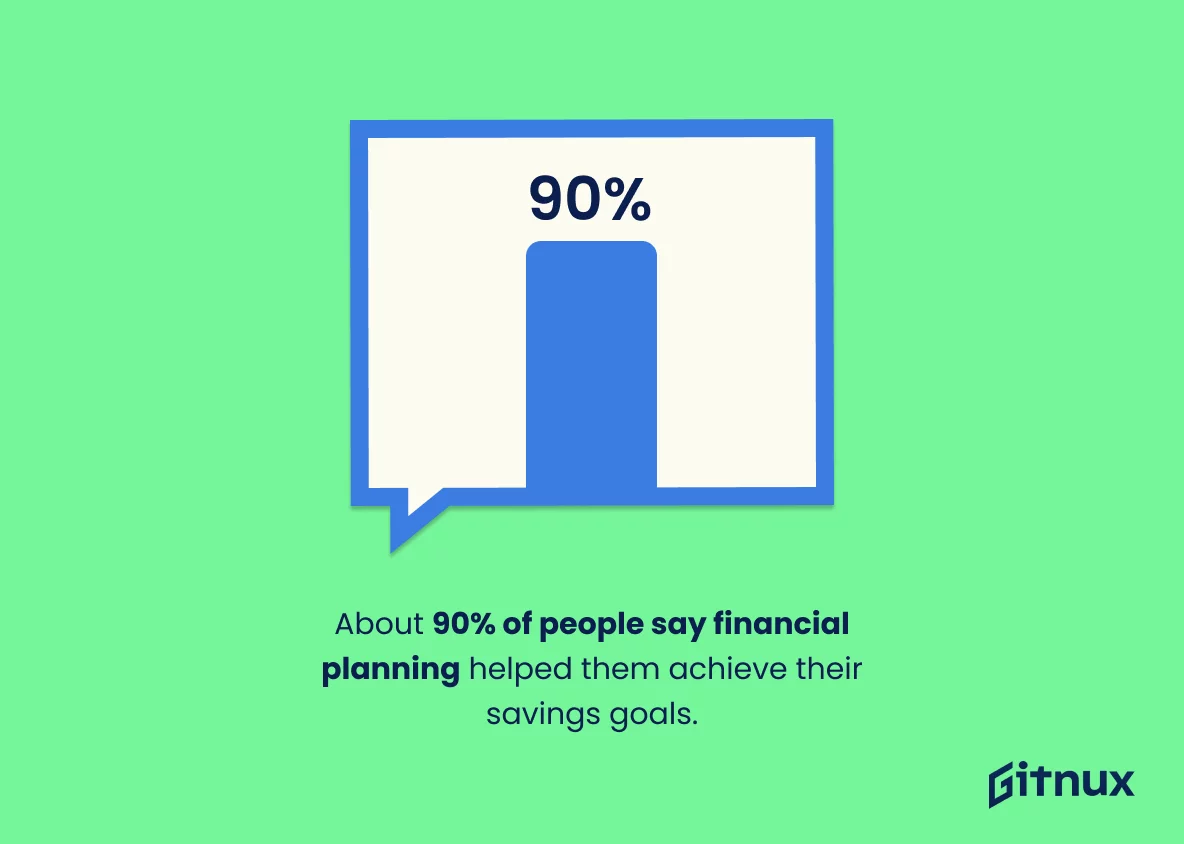

- Stat: A whopping 90% of individuals achieved their savings goals owing to comprehensive personal finance plans, emphasizing the necessity of a holistic service offering 6.

- Tip: Choose a planner offering a spectrum of services including retirement planning, estate planning, and risk management.

- Why is it important for a financial planner to offer a variety of services?A variety of services allows for a holistic approach to financial management, ensuring that all aspects of your financial life are considered and managed in a coordinated manner. This might include mutual funds, tax planning, and more.

- What is retirement planning, and why is it crucial?Retirement planning involves preparing for life after you stop working, which includes saving, investing, and making other financial arrangements to ensure a comfortable living post-retirement.

- What does estate planning entail?Estate planning involves the management and disposal of an individual's estate during their life and at and after death, while minimizing gift, estate, generation skipping transfer, and income tax.

- What is risk management in the context of financial planning?Risk management in financial planning refers to the identification, assessment, and strategizing to mitigate or manage financial risks that could negatively impact your financial situation.

Mistake 5: Underestimating Continuous Communication

- Stat: Clients report higher satisfaction levels with higher frequencies of investment-related educational communications and scheduled meetings, underscoring the importance of continuous communication 7.

- Tip: Ensure your financial planner maintains open channels of communication, keeping you informed and engaged throughout your financial journey.

- How can I ensure that my financial planner maintains open channels of communication?

You can set expectations for communication upfront, such as preferred methods of communication and frequency of updates. It's also helpful to choose a planner who is responsive and willing to engage in regular discussions about your financial plan. - Why is communication important in financial planning?

Communication is crucial to ensure that you and your financial planner are on the same page regarding your financial goals, risk tolerance, and any changes in your financial circumstances. It also helps in building trust and understanding throughout the financial planning process. - What are some red flags regarding communication with a financial planner?

Red flags could include lack of responsiveness, unwillingness to answer your questions, failure to provide clear explanations, or not initiating regular reviews and updates as agreed upon. - How can effective communication with a financial planner impact my financial journey?

Effective communication can lead to better understanding, trust, and alignment between you and your planner, which in turn can result in a more effective financial plan and a more satisfying financial journey.

Conclusion:

Avoiding these common pitfalls when choosing a financial planner can significantly steer your financial voyage towards success. Engaging with a reputable firm like Trilogy Financial not only helps sidestep these mistakes but also ensures a tailored, client-centric approach delivered by qualified professionals, fostering transparent communication throughout your financial journey1.