Introducing Financial Advisor Woburn

In Woburn, Massachusetts, financial advisors at Trilogy Financial Services, such as Tom Elkins, Dale Sarpard, and Mohammed Siddiqui, are guiding clients towards financial success with personalized investment strategies. Leveraging their collective expertise and local market understanding, these advisors offer unique insights into maximizing investments.

Understanding the Woburn Investment Landscape

The economic landscape of Woburn offers diverse investment opportunities. Advisors like Tom Elkins, an Accredited Investment Fiduciary, emphasize the importance of understanding local market trends and how they can impact investment choices. With their finger on the pulse of Woburn's economy, these advisors tailor their strategies to leverage local strengths. Some of these Key Strategies and Insights from Trilogy Financial Advisors include:

- Collaborative Strategy: Emphasizing a team-based approach, Trilogy Financial ensures clients benefit from diverse expertise and financial planning woburn.

- Comprehensive Solutions: By pooling the knowledge of various advisors, the firm can offer more holistic financial plans.

- Enhanced Understanding: This approach leads to a deeper comprehension of each client’s unique financial situation.

- Complex Situation Management: The collaborative effort of the team allows for effective management of intricate financial scenarios.

Tailored Investment Strategies

Each investor's journey is distinct, and advisors at Trilogy Financial Services recognize this. Dale Sarpard, with his extensive experience, illustrates the importance of creating investment plans that align with individual goals and life stages. From retirement planning to wealth management, their strategies are as unique as their clients.

Tom Elkins' Approach:

Tom Elkins' Approach:- Emphasis on understanding local market trends for informed investment decisions.

- Advocacy for personalized financial planning tailored to individual goals.

- Specialization in retirement planning and wealth management strategies.

Risk Management Techniques

Effective risk management is a cornerstone of successful investing. Mohammed Siddiqui, known for his client-focused approach, underscores the significance of a well-diversified portfolio. By balancing risk and return, these advisors help clients navigate market volatility with confidence.

Mohammed Siddiqui's Methodology:

- Prioritizing client-focused risk management and portfolio diversification.

- Adapting investment plans to changing market conditions and personal life changes.

- Utilizing technology for real-time investment insights and efficient planning.

Future-Proofing Your Investments

Woburn's financial advisors are adept at adapting investment strategies to evolving market conditions and personal circumstances. They prioritize long-term sustainability, ensuring that clients' investments can withstand economic shifts and personal life changes.

- Extensive experience in developing comprehensive financial plans.

- Focus on aligning investment strategies with life stage and financial objectives.

- Expertise in navigating complex financial scenarios for diverse client profiles.

Leveraging Technology for Investment Success

In today's digital age, technology plays a crucial role in investment management. Trilogy Financial Services utilizes advanced tools and platforms to provide clients with real-time insights and streamlined financial planning processes.

Conclusion

The advisors at Trilogy Financial Services in Woburn are committed to guiding clients through the complexities of investing. With personalized strategies, expert risk management, and sophisticated technology, they are equipped to help you achieve your financial goals. For those seeking to maximize their investments, consulting with these local experts is an invaluable step towards financial prosperity.

Ready to Amplify Your Wealth today?

If you're ready to elevate your financial planning with our professional team, we invite you to schedule a meeting with us. At Trilogy Financial Services, our advisors in Woburn are dedicated to crafting personalized financial strategies that align with your unique goals. Don't wait to start your journey towards financial success:

Schedule a Meeting: Reach out to us to arrange a one-on-one consultation with our financial professionals.

Give Us a Call: Prefer a quick conversation? Feel free to give us a call to discuss your financial needs and how we can assist. Call Us To Get Started. (844) 356-4934

Schedule a No-Strings-Attached Portfolio Review today and embark on a path to financial success guided by professional advisors. For more information and to schedule your consultation, visit www.trilogyfs.com/yourmoneyamplified. With the right knowledge and professional guidance, the journey of investing becomes an exciting venture towards achieving financial security and growth. This way, you're not just dreaming of an ideal retirement but actively working towards making it a reality.

*There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

Introducing Financial Advisor West Covina

In West Covina, California, a team of skilled financial advisors at Trilogy Financial Services, including Jeffrey Hackbarth, CFP®, Julie Foong, and Perry Johnson III, AIF®, is guiding clients toward financial prosperity with tailored investment strategies. These advisors, with their deep understanding of the local and broader financial markets, provide robust and insightful strategies to optimize investments. Their collective expertise offers a substantial advantage to clients looking to navigate the complex world of financial planning in West Covina.

Understanding the West Covina Financial Landscape

The financial landscape in West Covina, California, presents a range of investment opportunities, shaped by its unique economic factors. Trilogy Financial Services' advisors, such as Jeffrey Hackbarth, CFP®, place a strong emphasis on understanding these local market trends and their potential impact on investment choices. Their deep connection with the West Covina economy enables them to tailor their strategies effectively, ensuring they leverage local strengths to benefit their clients' financial objectives.Some of these Key Strategies and Insights from Trilogy Financial Advisors include Collaborative Strategy and Comprehensive Solutions:|

- Team-Based Approach: Highlighting a collaborative strategy, the West Covina office ensures clients benefit from the combined expertise of seasoned professionals.

- Personalized Financial Planning: The advisors offer custom solutions, taking into account each client's financial situation and objectives.

- Expert Management of Complex Financial Situations: The team's collective experience allows for effective management of a range of financial scenarios.

Tailored Investment Strategies

Each investor's journey is distinct, and advisors at Trilogy Financial Services recognize this. Jeffrey Hackbarth, with his extensive experience, illustrates the importance of creating investment plans that align with individual goals and life stages. From retirement planning to wealth management, their strategies are as unique as their clients.

Jeffrey Hackbarth, CFP®’s Expertise:

- Over 20 years of experience in wealth management and financial planning.

- Specialization in comprehensive wealth management, retirement planning, and family transition planning.

- Emphasis on building client trust through clear communication and personalized planning.

Risk Management Techniques

Effective risk management is a cornerstone of successful investing. Julie Foongi, known for her client-focused approach, underscores the significance of a well-diversified portfolio. By balancing risk and return, these advisors help clients navigate market volatility with confidence.

Julie Foong’s Approach:

- Combines creative financial planning with logical, goal-oriented strategies.

- Utilizes life insurance and managed investments as part of a holistic financial plan.

- Background in home loan consultancy, enriching her understanding of diverse financial needs.

Future-Proofing Your Investments

West Convia’s financial advisors are adept at adapting investment strategies to evolving market conditions and personal circumstances. Like Perry Johnson, they prioritize long-term sustainability, ensuring that clients' investments can withstand economic shifts and personal life changes.

Perry Johnson III, AIF®’s Methodology:

- Focuses on creating comprehensive and organized financial plans.

- Tailors strategies to encompass life goals and individual financial situations.

- Over 20 years of experience in the financial services industry, offering a holistic approach to planning.

Leveraging Technology for Investment Success

In today's digital age, technology plays a crucial role in investment management. Trilogy Financial Services utilizes advanced tools and platforms to provide clients with real-time insights and streamlined financial planning processes.

Conclusion

The advisors at Trilogy Financial Services in West Covina are committed to guiding clients through the complexities of investing. With personalized strategies, expert risk management, and sophisticated technology, they are equipped to help you achieve your financial goals. For those seeking to maximize their investments, consulting with these local experts is an invaluable step towards financial prosperity.

Ready to Amplify Your Wealth today?

If you're ready to elevate your financial planning with our professional team, we invite you to schedule a meeting with us. At Trilogy Financial Services, our advisors in West Covina are dedicated to crafting personalized financial strategies that align with your unique goals. Don't wait to start your journey towards financial success:

- Schedule a Meeting: Reach out to us to arrange a one-on-one consultation with our financial professionals.

- Give Us a Call: Prefer a quick conversation? Feel free to give us a call to discuss your financial needs and how we can assist. Call Us To Get Started. (844) 356-4934

Schedule a No-Strings-Attached Portfolio Review today and embark on a path to financial success guided by professional advisors. For more information and to schedule your consultation, visit www.trilogyfs.com/yourmoneyamplified. With the right knowledge and professional guidance, the journey of investing becomes an exciting venture towards achieving financial security and growth. This way, you're not just dreaming of an ideal retirement but actively working towards making it a reality.

*There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

Introduction:

Selecting a qualified financial planner is crucial for securing a robust financial future. A proficient planner, like those at Trilogy Financial, can create a financial plan tailored to your unique needs to help you reach your goals. Yet, a staggering 74% of Americans engage in financial planning without professional guidance, revealing a potential gap in making informed choices2.

Mistake 1: Overlooking Qualifications

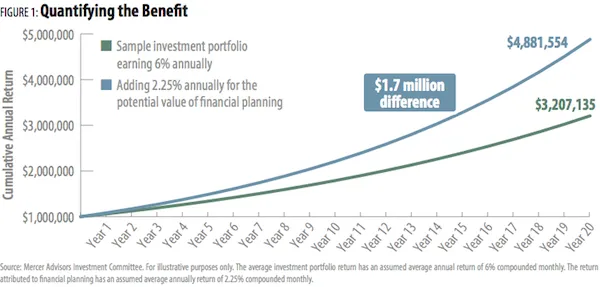

- Stat: Smart financial planning can yield 1.5% more in annual average returns, underlining the importance of qualified guidance3.

- Tip: When choosing an advisor ensure your planner holds pertinent certifications and showcases a robust track record of expertise.

- What are pertinent certifications for a financial planner?Pertinent certifications include the Certified Financial Planner (CFP), Chartered Financial Analyst (CFA), and Certified Public Accountant (CPA) designations. These certifications indicate a high level of expertise and adherence to industry standards.

- How can I verify a financial planner's certifications?You can verify a planner's certifications by checking the databases of certifying bodies like the CFP Board or the CFA Institute. Additionally, you can ask the planner for proof of certification.

- What constitutes a robust track record of expertise?A strong track record includes many years of experience, successful financial planning, happy clients, and industry recognition or awards.

- How can I assess a financial planner’s track record?You can assess a planner’s track record by reviewing client testimonials, checking for any industry awards or recognitions, and asking for references. Additionally, verifying their work history and experience in the field can provide insights into their expertise.

Mistake 2: Neglecting Fee Structures

- Stat: According to a 2019 Financial Trust Survey, “Nearly half of Americans (48%) incorrectly believe all financial advisers have a legal obligation to act in clients’ best interests.”4.

- Tip: Understand the fee structures and ensure transparency in your financial engagements if you chose to work with a financial advisor.

- What are common fee structures in financial planning?Common fee structures include fee-only (fixed, hourly, or percentage of assets managed), commission-based, and fee-based (a combination of fees and commissions).

- How can I ensure transparency in fee structures?Ask your financial planner for a clear, written explanation of all fees and charges, including any potential third-party fees, before engaging their services.

- What is the difference between fee-only and fee-based financial planners?Fee-only planners charge a flat fee, hourly rate, or percentage of assets managed, and do not receive commissions from selling financial products. Fee-based planners, on the other hand, may charge fees and also receive commissions, which could potentially lead to conflicts of interest.

- How do commissions affect the advice I receive?Commissions could potentially create a conflict of interest if a financial planner is incentivized to recommend certain products that earn them commissions, rather than what's in your best interest.

Mistake 3: Disregarding a Personalized Approach

- Stat: A Bankrate 2019 survey shows that 44% of individuals with a personal finance plan save more for retirement and 43% save 50% more per month.5

- Tip: When hiring a financial advisor opt for financial planners like those at Trilogy Financial, who prioritize a personalized approach to meet your unique financial objectives.

- What does a personalized approach in financial planning entail?A personalized approach means that the financial planner takes the time to understand your individual financial circumstances, goals, risk tolerance, and future aspirations to craft a strategy tailored to meet your unique needs.

- Why is a personalized approach important in financial planning?A personalized approach ensures that your financial plan is aligned with your goals and circumstances, which can lead to better financial outcomes and satisfaction over time.

- What are some examples of unique financial objectives that would benefit from a personalized approach?Unique financial objectives could include planning for early retirement, saving for a child's education, managing a large inheritance, or preparing for a significant life change like marriage or starting a business.

- How does a personalized approach compare to a one-size-fits-all approach in financial planning?A personalized approach provides tailored advice and strategies based on your individual circumstances, which can lead to more effective financial planning and better outcomes compared to a one-size-fits-all approach that may not align with your personal goals and risk tolerance.

Mistake 4: Ignoring a Comprehensive Service Offering

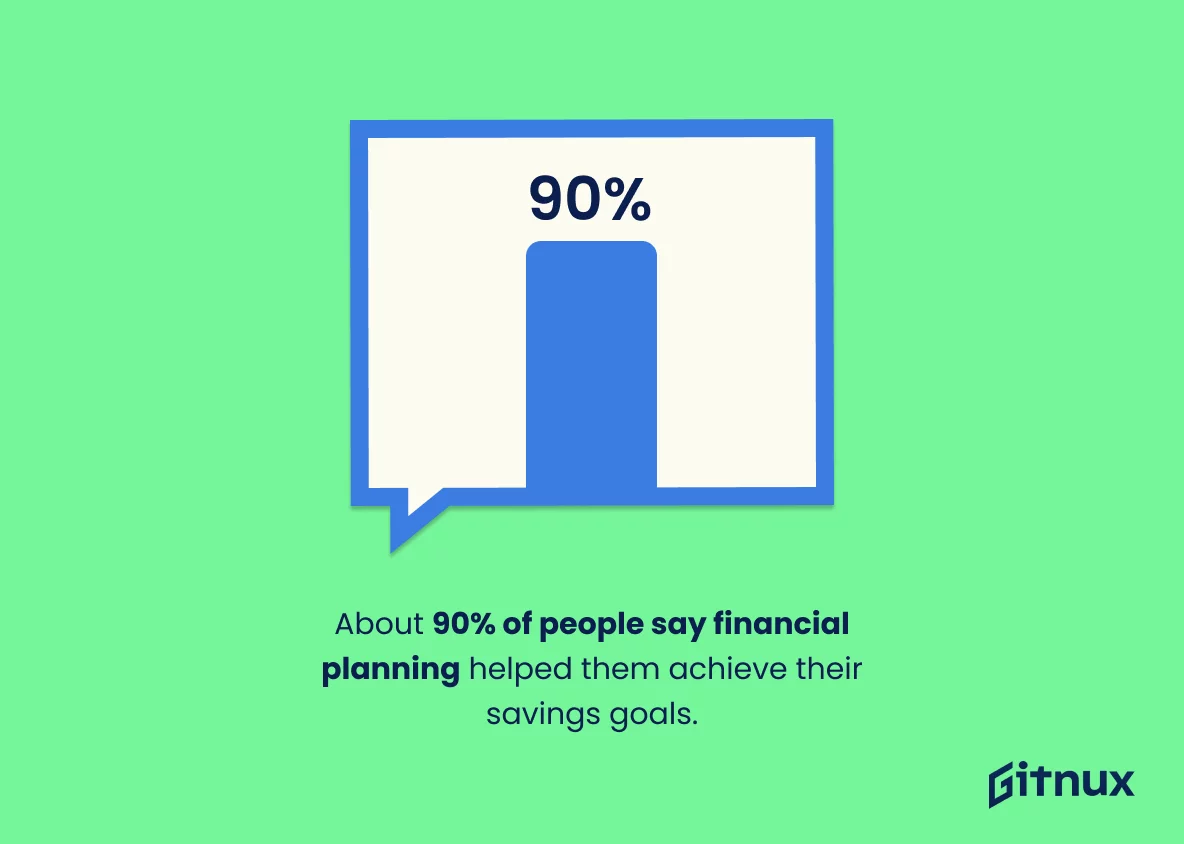

- Stat: A whopping 90% of individuals achieved their savings goals owing to comprehensive personal finance plans, emphasizing the necessity of a holistic service offering 6.

- Tip: Choose a planner offering a spectrum of services including retirement planning, estate planning, and risk management.

- Why is it important for a financial planner to offer a variety of services?A variety of services allows for a holistic approach to financial management, ensuring that all aspects of your financial life are considered and managed in a coordinated manner. This might include mutual funds, tax planning, and more.

- What is retirement planning, and why is it crucial?Retirement planning involves preparing for life after you stop working, which includes saving, investing, and making other financial arrangements to ensure a comfortable living post-retirement.

- What does estate planning entail?Estate planning involves the management and disposal of an individual's estate during their life and at and after death, while minimizing gift, estate, generation skipping transfer, and income tax.

- What is risk management in the context of financial planning?Risk management in financial planning refers to the identification, assessment, and strategizing to mitigate or manage financial risks that could negatively impact your financial situation.

Mistake 5: Underestimating Continuous Communication

- Stat: Clients report higher satisfaction levels with higher frequencies of investment-related educational communications and scheduled meetings, underscoring the importance of continuous communication 7.

- Tip: Ensure your financial planner maintains open channels of communication, keeping you informed and engaged throughout your financial journey.

- How can I ensure that my financial planner maintains open channels of communication?

You can set expectations for communication upfront, such as preferred methods of communication and frequency of updates. It's also helpful to choose a planner who is responsive and willing to engage in regular discussions about your financial plan. - Why is communication important in financial planning?

Communication is crucial to ensure that you and your financial planner are on the same page regarding your financial goals, risk tolerance, and any changes in your financial circumstances. It also helps in building trust and understanding throughout the financial planning process. - What are some red flags regarding communication with a financial planner?

Red flags could include lack of responsiveness, unwillingness to answer your questions, failure to provide clear explanations, or not initiating regular reviews and updates as agreed upon. - How can effective communication with a financial planner impact my financial journey?

Effective communication can lead to better understanding, trust, and alignment between you and your planner, which in turn can result in a more effective financial plan and a more satisfying financial journey.

Conclusion:

Avoiding these common pitfalls when choosing a financial planner can significantly steer your financial voyage towards success. Engaging with a reputable firm like Trilogy Financial not only helps sidestep these mistakes but also ensures a tailored, client-centric approach delivered by qualified professionals, fostering transparent communication throughout your financial journey1.

Have you ever envisioned a life of Financial Freedom and Leisure?

Have you ever envisioned a life where the chains of daily grind are broken well before the conventional retirement age, paving the way for a life of financial freedom and leisure? Embracing financial discipline and frugality can pave the way to a comfortable early retirement, answering the pressing question: Can meticulous financial planning and a frugal lifestyle significantly hasten your journey to early retirement?

What Makes Financial Planning Crucial?

Financial planning goes beyond merely saving a portion of your income; it's about understanding and rectifying financial bad habits that may impede your journey towards financial stability. Everyday financial misbehaviors such as impulsive spending, credit card debt, and the lack of a structured financial plan for emergencies often go unnoticed but have a long-term detrimental impact on financial health. Addressing these personal finance habits is the first step in financial planning.

- Why is Debt Management Essential? A key aspect of financial planning involves managing or eliminating debt, which can otherwise consume a significant portion of your income in the form of interest payments.

- Did you know in the US for 50-59-year-olds the average debt is $23,719 1.

- How Can Budgeting Secure Your Financial Future? Being unsure of where your money is going is a red flag. Budgeting is crucial to track and control spending, ensuring your expenditures align with your values.

- Did you know the average individual aged between 65 to 74 spends about $55,000 on living expenses annually2.

- How do Savings and Investments Impact Your Retirement Goals? Setting aside money for an emergency fund and future investments is essential. Automating this process by having a portion of your income transferred to savings or investment accounts can help in cultivating this good financial habit.

What Does Adopting a Frugal Lifestyle Entail?

Frugality is about making informed and restrained financial decisions to save money. A frugal lifestyle encourages avoiding unnecessary expenses and finding value in what you spend.

- Examples of frugal practices include avoiding spending triggers like malls or online shopping platforms, utilizing cash over credit to prevent overspending, and finding cost-effective alternatives for everyday expenses.

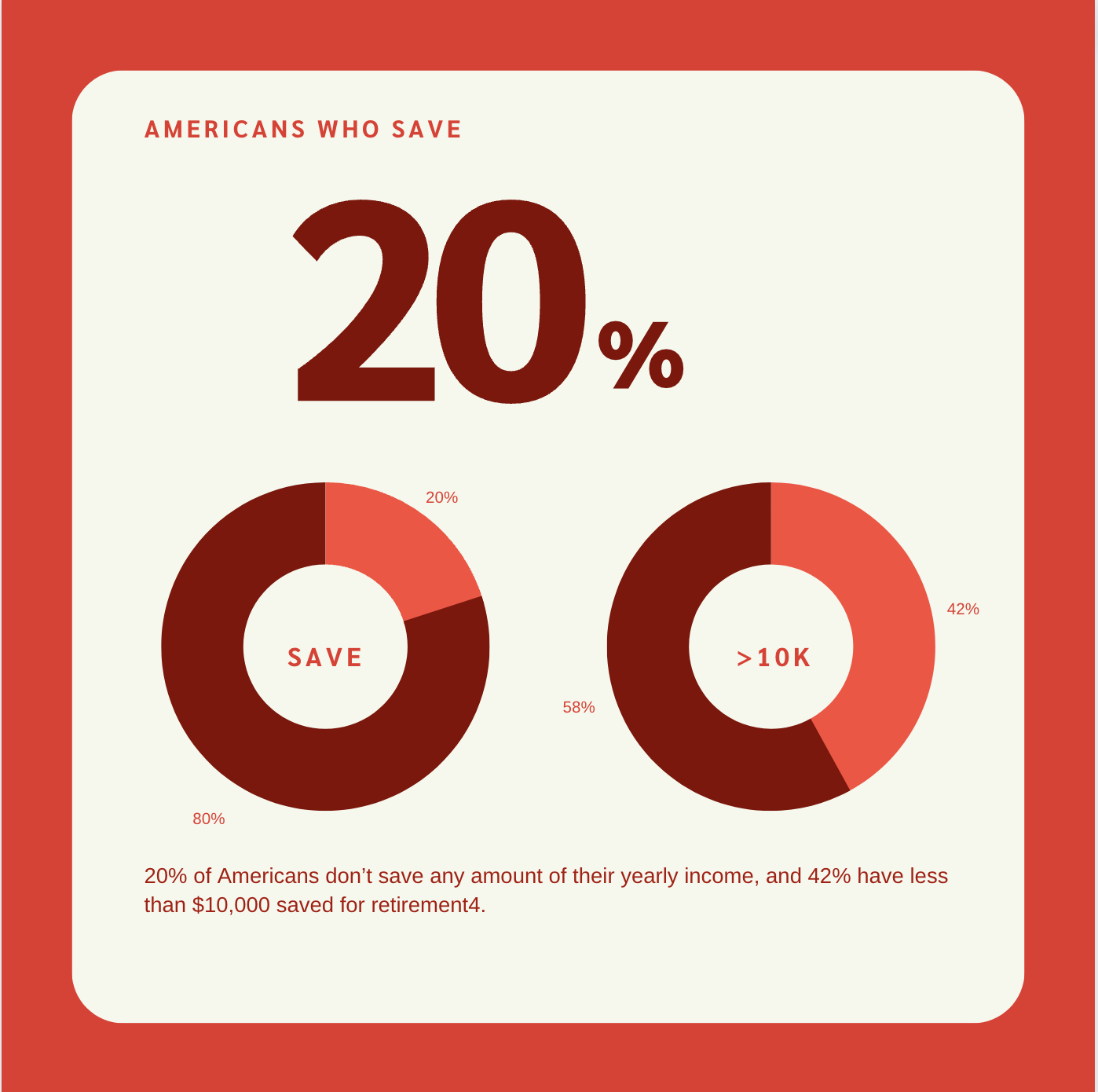

Did you know 20% of Americans don’t save any amount of their yearly income, and 42% have less than $10,000 saved for retirement4.

What are the Key Components of Financial Planning for Early Retirement?

- Emergency Fund: Ensuring you have an emergency fund can help buffer against unforeseen circumstances like a job loss or medical crisis, which might otherwise derail your financial plans.

- Investment Strategy: Diversifying your investments and aligning them with your retirement goals is imperative for financial growth.

- 84% of Americans have a higher income than their parents did at the same age, indicating potential for savings and investment if managed wisely4.

- Tax Planning: Efficient tax planning can help in preserving your wealth and ensuring more of your money is working for you rather than going towards taxes.

- Healthcare Planning: As healthcare costs can be exorbitant, planning for these expenses is crucial to avoid financial strain in later years.

- Healthcare can be a significant part of living expenses, as seen in the $55,000 annual spending for individuals aged 65-745.

Which Tools and Resources Can Aid Your Financial Planning Journey?

There are myriad tools and resources available to aid in your financial planning journey. Budgeting apps, financial advisors, and online courses are excellent resources. Trilogy Financial, for instance, offers a Decision Coach program designed to provide additional accountability and coaching to individuals seeking financial guidance.

- 37% of workers aged 25 and older, and 19% of retirees, report not knowing where to go for financial or retirement planning advice5.

Easily Meet with a Certified Financial Planner.

How Have Others Achieved Financial Independence and Early Retirement?

The quest for early retirement often begins with a thorough re-evaluation of one's financial plan, identifying areas of improvement, and capitalizing on unforeseen savings opportunities. The year 2020 saw many Americans saving more, with an average of 10% more money saved compared to 2019, mainly due to lifestyle changes induced by the pandemic. Some redirected these savings towards home improvements, while others saw it as a stepping stone towards drafting a solid financial plan aimed at debt reduction, college planning, or accelerating the journey to financial independence.

Various individuals and communities dedicated to frugal living and meticulous financial planning have emerged over the years, showcasing diverse pathways to early retirement. Here are a few noteworthy examples:

- Juan's Early Retirement Ambition: Juan, an aspiring early retiree, aimed to bid farewell to his federal job by 2031 at the age of 43. His strategy revolved around living off savings, investments, and dividends post-retirement to enjoy more time with family and delve into philanthropic ventures. Though new to the Financial Independence, Retire Early (FIRE) movement, Juan's no debt and $85,000 asset accumulation puts him in a favorable position towards achieving his goal1.

- The FIRE Movement: The Financial Independence, Retire Early (FIRE) community exemplifies the synergy between frugal living and early retirement. Members of this movement, like Juan, embody a lifestyle of extreme savings and frugality, aiming to retire much earlier than the conventional age2.

- Young Adults Eyeing Early Retirement: The allure of early retirement isn't confined to older age groups. One in four individuals between 18 to 34 years old has set early retirement as their significant financial milestone, driven by the principles of frugal living and meticulous financial planning3.

- A 5-Year Transition Plan: A couple outlines their 5-year plan towards financial independence, with one partner continuing full-time work for an additional 3-4 years, demonstrating a balanced approach to achieving early retirement while maintaining a comfortable lifestyle4.

- Frugal Living as a Fast Track to Early Retirement: The narrative of saving 75% of income, a hallmark of frugal living, expedites the journey towards early retirement, allowing individuals to accumulate substantial savings, invest wisely, and achieve financial independence sooner5.

These cases highlight the transformative impact of frugal living and prudent financial planning to achieve early retirement dreams. They speak to the importance of continuous financial plan evaluation, adapting to changing circumstances, and leveraging savings opportunities to expedite the journey to financial independence and early retirement.

Conclusion:

The road to early retirement is laden with challenges, primarily stemming from our own financial bad habits. However, if we create a financial plan, adopt a frugal lifestyle, and leverage available resources, overcoming these challenges and retiring early is an achievable goal.

Discover how working with a financial planner can make a big difference in your investing journey. Learn about investing through our beginner's guide to top investment blogs.

For many, investing seems like a daunting venture. Navigating through the intricacies of the financial world can be overwhelming, especially when you're just starting out. But beyond the stock market fluctuations and intricate charts, it's essential to grasp your financial aspirations.

Warren Buffett wisely said, “Don't save what is left after spending, but spend what is left after saving.” This highlights the importance of financial planning and goal setting when it comes to investing.

As emphasized by Jeff Motske, CFP® at Trilogy Financial Services, understanding your financial “why” is just as pivotal. Are you eyeing retirement? Or maybe that dream home or a new startup? These goals should shape your long term investment journey.

To help beginners transition into the investment realm, here's a two-fold strategy:

1. Consult a Financial Planner or Advisor

Engaging with a financial planner or advisor is akin to having a personalized coach for your financial journey. Just as you wouldn't start an intense workout regimen without gauging your physical limits, investing without a clear vision of your financial goals and investment decisions is risky.

A financial planner will assist in evaluating your risk tolerance—an essential element in devising an investment strategy. As Peter Lynch, a renowned investor, once remarked, “Know what you own, and know why you own it.” This stresses how important it is to be informed and understand one's investments.

2. Discover the Top Investment Blog Posts for Beginners

In Personal Finance, staying on top of your investment portfolio starts with understanding continuous learning is a key ally in the world of investments. Here are some top investment blogs for beginner investors that can offer invaluable insights:

- Investopedia: A comprehensive platform offering a plethora of articles, tutorials, and educational content on finance and investment.

- The Motley Fool: A trusted source renowned for its stock recommendations and investment advice, catering to both novices and seasoned investors.

- Seeking Alpha: A blend of free and premium content, providing in-depth research, articles, and analyses on various stocks and investment strategies.

- BiggerPockets: The go-to resource for real estate investment enthusiasts, packed with guides, resources, and community discussions.

- NerdWallet's Investing Section: Simplifies complex investment topics, making them digestible for beginners.

- Nasdaq News + Insights: Get insights from a big stock exchange. Covers market trends, stock market news & analysis, and investment strategies.

- Morningstar: This blog is a trusted source for investment research. It provides analysis, ratings, and information on stocks, mutual funds, and ETFs. This makes it important for both new and experienced investors.

Conclusion

Stepping into the investment arena can evoke a mix of emotions. But as you start investing with a clear understanding of your financial goals, expert advice, and regular insights from top investment blogs for beginners, you're on a solid path.

As Benjamin Graham, known as the “father of value investing,” once said, “The individual investor should act consistently as an investor and not as a speculator.”

At the end of the day it's important to ensure you make informed, strategic investing over impulsive decisions. Check out how to avoid Mistakes When Choosing a Financial Planner in our other blog post.

Keen on diving deeper into investing? Connect with our top financial planners or explore more articles on our investment blogs for investment strategies.

As the cost of living rises, households worldwide feel the squeeze. Inflation impacts everything from groceries to housing to healthcare, and families struggle to make ends meet as they stretch their budgets to the limit.

Recent statistics show the inflation rate in the United States has risen to its highest level in over four decades. The Consumer Price Index (CPI) has increased by 7% over the past year alone. Inflation is a persistent increase in the prices of goods and services over time, leading to a decline in purchasing power of money. It affects the economy in many ways, including households, as it erodes their buying power, making it difficult to afford basic necessities.

How Is Inflation Impacting Households Today?

Inflation is affecting families significantly, with prices of goods and services rising rapidly. One area where inflation has a noticeable impact is the cost of groceries. According to the U.S. Department of Agriculture, food prices have increased by 6% in the past year.

Inflation is also impacting the cost of housing. According to the National Association of Home Builders, lumber has increased by more than 167% since April 2020, making building, renting or renovating homes much more expensive.

Other areas where inflation impacts households include transportation, healthcare and energy costs. With gas prices rising, transportation costs are increasing making it more expensive for families to commute to work or travel.

Healthcare costs are also rising, with medical services and prescription drugs becoming more expensive daily. Additionally, the cost of energy, including electricity and natural gas, is increasing impacting household budgets.

How We Got Here and Why?

The United States has experienced an increase in inflation in recent years, fueled by a combination of factors, including:

Supply chain disruptions: The COVID-19 pandemic caused disruptions in supply chains, leading to shortages of goods and raw materials and higher consumer prices.

Government stimulus: The US government has implemented several rounds of stimulus packages in response to the pandemic, flooding the economy with cash and contributing to inflation.

Labor shortages: The pandemic also caused labor shortages in many industries, which has led to increased wages for workers and higher prices for consumers.

Rising energy costs: The cost of energy has increased, with higher prices for gasoline and other commodities, which has increased the cost of goods and services.

Monetary policy: The Federal Reserve has kept interest rates low to stimulate economic growth, contributing to inflation by making it cheaper for consumers and businesses to borrow money.

These factors have all contributed to the current state of inflation in the US. However, inflation is complex and multifaceted; many other factors are also at play.

7 Tips to Help Navigate Inflation

Inflation can be a challenging economic environment for households to navigate. Here are tips from our team of advisors at Trilogy Financial that can help you manage inflationary pressures.

1. Calculate Your Inflation Rate

This measure provides a more accurate reflection of the inflation you are experiencing compared to the general inflation rate reported in the media.

A financial advisor can help calculate your personal inflation rate by analyzing your spending habits and identifying the goods and services that make up your personal consumption basket. This process can involve reviewing bank and credit card statements, examining household bills, and discussing significant lifestyle or spending habits changes to help you track the prices of these items over time and calculate your inflation rate.

2. Create a Cash Management Strategy

A cash management strategy will allow you to preserve your purchasing power and financial stability. A financial advisor can help you create a strategy that aligns with your financial goals and risk tolerance by:

- Assessing your current financial situation,

- Identifying your short-term and long-term cash needs, and

- Recommending appropriate investments that balance liquidity, yield, and risk.

The strategy can involve diversifying cash holdings across different asset classes, using inflation-indexed bonds or money market funds, and considering alternative investments that offer potential inflation protection.

3. Discuss When and How to Use TIPS to Protect Against Inflation

Treasury Inflation-Protected Securities (TIPS) are a type of U.S. government bond indexed to inflation. As inflation rises, the principal and interest payments of TIPS adjust accordingly, providing investors with a hedge against inflation. A financial advisor may recommend TIPS if you want to protect your portfolio against inflationary pressures or maintain your purchasing power over the long term. It could involve assessing your risk tolerance and investment objectives and recommending an appropriate allocation to TIPS within a diversified portfolio.

4. Discuss Alternative ‘Inflation-Hedging' Assets

In addition to TIPS, assets such as commodities, real estate and stocks of companies with pricing power can provide inflation protection. A financial advisor can help you choose the right assets for your portfolio by assessing your investment objectives, risk tolerance and time horizon. As a result, they can recommend an appropriate allocation to inflation-hedging assets that balance return and risk, like commodity funds, real estate investment trusts (REITs) or sector ETFs offering exposure to companies with pricing power.

5. Strategize for How to Avoid ‘Tax Bracket Creep' as Income Rises

Tax bracket creep pushes an individual's income into a higher tax bracket, resulting in a higher tax bill. This move can erode the purchasing power of your income and reduce your savings.

A financial advisor can help you strategize on how to avoid tax bracket creep by considering tax-efficient investment vehicles, such as Roth IRAs, tax-loss harvesting and charitable donations.

6. Review Homeowners and Other Insurance Solutions to Avoid Under Coverage

As the value of assets, goods and services increase due to inflation, the cost of replacing them also rises. A financial advisor can help you review your insurance coverage and ensure they have inflation protection from risks.

Advisors can also educate you on the different types of insurance available and their benefits, such as umbrella insurance, which can provide additional liability coverage in case of a significant lawsuit or accident.

7. Reassess Long-Term Inflation Assumptions for Retirement Projections

Inflation can significantly impact retirement savings and planning because it reduces the purchasing power of money over time. Individuals will need to save more to maintain their living standards in retirement.

A financial advisor can help you reassess your long-term inflation assumptions for retirement projections by analyzing your current savings and investment strategies, projecting future inflation rates, and identifying potential gaps in your retirement plans.

From Us to You: Control Your Financial Future

As inflation continues to affect households, you should take control of your financial situation and work with a financial advisor to develop a plan aligning with your goals, risk tolerance and personal situation.

Trilogy Financial is a financial advisory firm dedicated to helping clients navigate the complex world of personal finance. We offer comprehensive services, including financial planning, investment management, and retirement planning.

If you are concerned about the impact of inflation on your finances, contact us today to schedule a consultation with one of our experienced advisors. We are here to help you take control of your financial situation and navigate through the challenges of inflation.

__________________________________________________________________________________________________________________

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual 2. Investing involves risk, including possible loss of principal.

Planning for retirement amid changing market dynamics can be stressful, especially as retirement age approaches. Fortunately, there are a myriad of ways to prepare for it, even if you plan to retire early.

OPTIMIZE YOUR RETIREMENT INCOME

One of our top tips is to optimize your retirement income by setting yourself up with a diversified portfolio that offers a solid return. If you are in your twenties, there is a big opportunity to let compound interest work its magic. If you are in your thirties or forties, compound interest may not be as lucrative for you, but there are still plenty of ways to maximize your returns.

Here are some of the different options available to help plan for retirement:

- SEP IRA – a self-employed retirement plan known as the Simplified Employee Pension (SEP) IRA requires employers to contribute 100% of the accounts' funds and provide equal benefits to all eligible employees.

- 401(k) – An individual retirement plan for which contributions are not tax-deductible, but withdrawals in retirement are tax-free.

- Roth IRA – An individual retirement plan for which contributions are not tax-deductible, but withdrawals in retirement are tax-free.

Each option has its differences, so it is important to work with an advisor to identify which is best suited to your situation and your goals. There’s a lot that can go into your Life Plan and we are here to help.

DEVELOP A BUDGET AND SAVINGS PLAN

Budgeting can make a world of difference. If you haven’t already, establish an emergency fund. This will give you peace of mind and will help pay for any unexpected expenses that may arise. Once you’ve set that money aside, you can plan your monthly expenses, retirement contributions and more with the rest of the income you have.

As you develop this budget and savings plan to get you to your retirement goals, ask yourself the following questions:

- What quality of life do I want to experience in retirement?

- What medical expenses do I anticipate?

- Do I plan on working during retirement?

- Will I have a flow of income during retirement?

These are all important considerations and will help you develop an actionable plan to achieve the retirement lifestyle you dream of.

DETERMINE YOUR TAX BRACKET AND MINIMIZE YOUR TAXES

In retirement, taxes can eat into your available income, leaving you with less to live on. It's important to remember that taxes don't stop once you're retired. Our financial advisors are here to help guide you take steps throughout your working life to minimize your IRS obligations now and later.

The same basic tax brackets that apply to working taxpayers also apply to retirees. Determining your tax bracket in retirement is just like determining your tax bracket while you’re working – which is determined by your filing status and taxable income (income minus deductions).

Common sources of retirement income that are taxable include:

- Distributions from traditional 401(k)s and IRAs

- Investment income

- A portion of your Social Security benefits (in some situations)

- Some pension income

- Income from work (full or part time)

INVEST TO ADD ADDITIONAL CASH FLOW IN RETIREMENT

If building wealth is your goal, the stock market or other investment strategies are common options. Investments such as annuities, real estate investment trusts (REITs) and income-producing equities can offer additional retirement income beyond Social Security, a pension, savings and other investments.

DETERMINE THE AMOUNT OF RISK THAT IS APPROPRIATE FOR YOU

It is important to keep in mind that all investments come with risk. If you are young, you can probably tolerate more risk. If you are in your thirties or forties, however, you might benefit from taking a lower risk approach. This is because people in their twenties have more time to correct and mitigate losses. A financial advisor can help you decide if you would like to take a low-risk, slow-and-steady approach, or guide you through a high-risk approach with the potential of yielding higher returns.

PAY OFF YOUR DEBTS

It’s important to pay off credit card debt and student loans as soon as possible. Systematically chipping away at debt now, can have a significant impact on your future debts and purchasing power.

A mortgage can be looked at as both a good debt and a bad debt, depending on your goals. Many people choose to rent a home to avoid being tied to a mortgage, and others use that property as a cash-positive asset. Depending on your goals, it’s important to discuss each of these approaches with a financial advisor so they can help guide you through something that will ultimately benefit you and your family.

MAXIMIZE YOUR SOCIAL SECURITY BENEFITS

Navigating Social Security income can be complicated, but there are several ways to maximize your social security benefits, including:

- Work for 35 years or more

- Earn as much as you can right up until full retirement age (or past it)

- If you can, wait until you are 70 years old to claim – this can increase your benefit by 8% a year beyond your full retirement age

The goal is to maximize the income you will receive from Social Security, but the answer for you will depend on your age, current income, marital status, spouse’s income, and the age disparity between you and your spouse. With all the complexities to Social Security planning, there is no substitute for meeting with a trusted financial advisor so you can best navigate your life in retirement.

CONSIDER ESTABLISHING STREAMS OF PASSIVE INCOME

It's important to remember that there are multiple ways to set yourself up for prosperity during your golden years.

These include:

- Investing in real estate

- Investing in the stock market

- Starting an ecommerce business

- Writing books

- Earning royalties of any kind

- Investing in collectibles

- Investing in gold and silver

In short, it's best to invest in as many financial assets as you possibly can in order to establish streams of passive income so that you are not solely reliant on one source for your earnings and returns.

ESTABLISH MULTIPLE STREAMS OF INCOME

You may want to consider continuing to work during retirement. This provides many people with a sense of satisfaction and purpose, AND you will be able to keep your benefits.

The earlier you establish multiple sources of income the better. Ideally, at least a few of these would be passive.

You deserve to be comfortable during retirement, and planning for this phase of life right now will likely help you achieve your goals, perhaps even surpass them. You have worked hard for most of your years around the sun, and you deserve to relax and enjoy every moment on your own terms during your golden years.

Why Choose Trilogy Financial

Planning your retirement strategy is important but not something to stress over. If you’ve already started saving, one of our certified financial planners can help you optimize your savings, investing and risk approach so you can live the retirement life you dream. However, if you haven’t started planning for retirement yet, there’s no better day than today!

Our Advisors will work with you to develop a deeper understanding of your alternatives, pinpoint practical needs and make plans for the care you and your family deserve. Please contact us to start your retirement planning today.

Financial planning involves thoughtfully outlining objectives and setting goals in your Life Plan. With anything, the possibility of running into obstacles, options, and challenges throughout your financial journey is unavoidable. That’s why it is important to implement some sort of checks and balances to mitigate these challenges. Insurance is one of the best ways to account for unforeseen conditions and events in your financial plan. The thought of utilizing insurance can be daunting. It makes the possibility of losing your car or home due to an accident, flood, or fire a reality. That’s exactly why we create a financial plan – to be prepared for the unexpected. Our team is committed to coaching you through the process, so that you can make an informed and confident decision. There are various types of insurance services available that your Trilogy Financial advisor can help you navigate so you can handle the many uncertainties that life throws your way.

Read on to discover these insurance services.

Insurance Services Provided by Trilogy Financial

Every Trilogy Financial Advisor is committed to helping you build the legacy you have always desired to leave through the following services:

Term Insurance

A term insurance policy is the most common form of temporary life insurance. The term usually lasts for a specific “term” of years. Term insurance is also a form of insurance that is rented. Meaning, you pay a monthly premium for the insurance, but it expires after the allotted time frame. The duration can range from five to thirty years.

Term insurance protects liabilities that will cease to exist after a specific period, such as providing extra cashflow for raising children. It is a simple life insurance plan that protects against the possibility of an untimely death. A death benefit is granted if the insured passes away during the policy's stated tenure.

Because death is unpredictable, term insurance plans are essential. The family may experience a significant financial loss if the family's primary provider passes away. A term plan covers the loss. It benefits the family, allowing them to cover lifestyle costs and continue to address their financial objectives.

Permanent Insurance

Permanent insurance can be considered “owning” insurance coverage. Like term insurance, you pay a monthly premium; however, in permanent insurance, the range is continuous and does not end within a time frame.

For instance, even after your children have moved out and your liabilities have diminished, you may continue to carry some form of insurance to cover your loved ones and compensate for your end-of-life needs.

Permanent insurance premiums are more significant than term insurance premiums because, unlike term insurance, the insurance company may never have to pay out the policy. Permanent insurance can be used as an income and an insurance tool. Both a death benefit and a cash value factor are included. You can access the money as the value increases by taking out a loan or a withdrawal, and you can terminate the insurance by withdrawing the cash value.

Long-Term Care Planning

Long-term care planning, at its foundation, entails ensuring that you or a loved one's needs are adequately met when they can no longer care for themselves. Therefore, as you age, having a practical plan becomes more and more crucial. While many maintain their independence well into their senior years, it never hurts to plan.

Any long-term financial plan should consider long-term care costs, especially if you are in your 50s or older. You are unlikely to qualify for long-term care insurance if you already have a disabling condition. Most over 75 applicants will not be accepted by long-term care insurance providers. Most persons who purchase long-term care insurance do so between 50 and 60.

Risk Management

Risk management entails recognizing, assessing and managing risk. A well-executed risk management program is built on a foundation of standardized risk assessments to assist businesses in prioritizing their risk based on its potential impact. This procedure will inevitably reveal hazards affecting the company's fundamental competencies.

As financial Advisors, it is a part of our job to help you navigate your financial well-being, which includes helping you mitigating certain risks. Identifying your risk factors is your first defense, followed by avoiding or limiting risks to your income and survivors. Insurance is your quality line of defense.

Importance of Insurance in Financial Planning

Here are some factors that make insurance an essential aspect of your Life Plan:

- Financial assurance: You feel safe knowing that the insurance policy will cover the damages in the event of an emergency.

- Tax advantages: Insurance lowers your taxable income and provides financial benefits.1

- Risk protection: Insurance prepares you to deal with any financial loss you might suffer in the event of an unplanned circumstance.

- Meeting your prerequisites: Several insurance policies are available to cover the various risks you can encounter.

- Peace of mind: Insurance plans assure you that your funds will not be compromised in the event of an emergency.

*This information is not intended as authoritative guidance or tax advice. You should consult with your tax advisor for guidance on your specific situation.

Why Choose Trilogy Financial

Your financial plan should be strategically in line with your insurance. Our Trilogy Financial Advisors use a comprehensive strategy to offer insurance policies tailored to your specific needs and Life Plan. We understand the risks you face and how to help improve your financial life. Our Advisors will work with you to develop a deeper understanding of your alternatives, pinpoint practical needs and make plans for the care you and your family deserve.

To help you build the life you’ve dreamed, we collaborate with the most reliable insurance firms with a track record of being financial secure and capable of paying claims.

Get Started with a Financial Advisor Today

Everyone has a distinct level of risk, and before purchasing insurance, it is critical to identify risks and establish how to limit the likelihood of them occurring. We understand that everyone has a varying level of comfort and experience in navigating finances and Life Plans. That’s why our Advisors are committed to being both a partner and coach to support you as much or as little as you need, so you can make the best decisions for you and your family.

At Trilogy Financial, our Advisors will guide you through your daily financial decisions to keep you on track and set you up for your real-life goals. If you have any questions concerning insurance or any other element of your financial life, get in touch or visit our website today to book a meeting with an advisor

Estate planning is an essential step to help protect the wealth that you've spent your life building. Meeting with an estate planner will help to create a comprehensive plan that will allow your assets to effectively pass to your assigned beneficiaries. Creating this initial plan can feel overwhelming, and we are here to help you prepare.

Here are five important questions you can expect to discuss with your estate advisor as you start to plan for your future.

How Would You Like Your Wealth to Pass to Your Heirs or Elsewhere?

The basis of your estate plan is where you want to direct your wealth and how you'd like that to happen. No matter how large or small your estate is, you'll need to decide how it should be distributed among children, grandchildren, other family members or favorite charity organizations. For example, this could mean leaving different parties a percentage of your total assets, or leaving one child your business and another child your vacation home.

It’s important to also think about whether you want your beneficiaries to receive their inheritance all at once or not. If you have a disabled child requiring lifelong care on your list, or someone who needs a little extra help managing their money, you may want a trust or annuity structure in place to pay out the inheritance in increments.

What Can Be Done to Prevent Costs and Conflicts for Your Heirs?

Costs for your beneficiaries are most likely to come up if your estate needs to go through probate, which is the process by which a court distributes your assets. In addition to financial costs, there are other reasons to avoid probate. Probate can be a long and exhausting process – meaning, your heirs will not be able to access your estate right away. If you have dependents who will rely on the money in your estate, this can be an especially serious concern. In addition, probate adds your estate information to the public record, which you may want to avoid. There are several strategies your financial advisor might recommend to avoid probate. These include placing assets in a trust and moving funds into joint accounts with your beneficiaries.

Conflict among heirs is another common concern, especially in families where conflict already exists. While the legal documents included in your estate should help minimize disagreements and make it more difficult for someone to contest your wishes, communication during your lifetime is important as well. Disagreements often surround specific items like jewelry or sentimental pieces rather than your financial assets. Labeling these items, writing a letter of instruction and starting to pass on these things during your lifetime can all help make your intentions clear.

How Can You Reduce Your Tax Burden?

After a lifetime of working to earn your money, you likely want to direct your wealth to your loved ones rather than the government. In 2023, only estates valued at $12.92 million (or $25.84 million for some married couples) or more may be subject to the federal estate tax. If, upon your death, the total value of your estate is less than the applicable exclusion amount, no federal estate taxes will be due.

Depending on the state you live in, your heirs or your estate might also be subject to state estate or inheritance taxes. If taxes are a concern for your estate, there are several ways to reduce your tax burden.

One simple option is to start passing money along during your lifetime. Based on the 2022 gift tax exemption limit, individuals can give up to $16,000 per recipient per year. This lets you give money directly to your children or grandchildren while reducing the value of your estate, which will reduce your tax bill. Other options include a marital trust, which allows one spouse to place assets in trust for the other spouse, and an irrevocable life insurance trust, which can pay for life insurance premiums with tax-deductible funds and then avoid estate taxes later on.

Are You Already Working with Financial Professionals?

If you're already working with an estate attorney, a financial planner or a tax professional, it's important for your estate planner to understand the strategies your existing financial team has recommended. You'll want to make sure that all of these members of your team are working together so you aren't paying for duplicated efforts or conflicting suggestions.

If you aren't already working with a financial team, your estate planner may recommend that you do so depending on the details of your estate plan. If you have complex tax concerns, you might need to talk to a tax expert. Depending on the type of trust that you wish to establish, you may need an estate attorney to set it up.

How Will Changes in Your Life Change Your Estate Plan?

Your estate plan should have the flexibility to adapt to changes in your lifestyle, family structure or life expectancy. Your initial plan will be based on your current circumstances, but you should consider potential future concerns and possible solutions.

Divorce and Remarriage

Divorce and remarriage are common life changes that can affect your estate plan. If you remarry, you may not want your new spouse to manage the inheritance of your children from the first marriage. This can create the need for a new trust to be established. In addition, if you have more children in later marriages, you will again need to update your estate plan.

Life Expectancy and Medical Issues

There are other lifestyle considerations that might change as well. For example, if based on your family history you expect to live into your 90s, you might not want to start giving away assets to avoid estate taxes. And if medical issues arise and your life expectancy changes, you will likely need to adjust your plan.

While you won't need to make any decisions based on hypotheticals, it's a good idea to discuss the possibilities.

How to Get Started?

Your estate plan is a key component of your Life Plan. To create an estate plan that addresses the above questions and any other concerns you may have, you'll need to start by finding the right estate advisor. Talk to the Trilogy Financial team to take control of your finances today while maximizing your future opportunities.

Download your free Estate Strategies eBook to learn how to protect your estate.

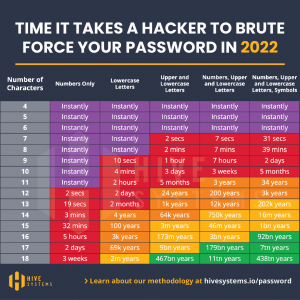

How long do you think it would take a hacker to crack your current passwords?

On average, it takes a hacker about 2 seconds to crack an 11-character password that only uses numbers. See the attached chart that illustrates the time it takes for a hacker to brute force attack your password. A brute force attack is when cybercriminals use trial and error to guess your details. Cybercriminals currently use sophisticated software that can run thousands of password combinations in a minute, but their technology and resources are only getting stronger.

A general rule is that your password should be at least 11 characters, utilizing both numbers as well as upper and lowercase letters. That combination will take hackers 41 years to crack. Regardless of the possible variations, the shorter your password, the easier it is to crack. Check out how long it will take a hacker to crack your password at https://www.security.org/how-secure-is-my-password/.

Lastly, simplify and secure your accounts by using a password manager that creates and stores all your passwords for you.

Strengthen your password security with the following tips:

- Prioritize the length and complexity of your passwords.

- Don't use personal information. This can be publicly available and easily accessible by hackers.

- Avoid using dictionary words as passwords. Cracking tools can easily process every word in the dictionary.

- Don't reuse passwords. If one account is breached, your other accounts would be vulnerable as well. Rather, use password managers, which are a convenient and secure way to manage complex passwords on multiple platforms.

- Use multifactor authentication (MFA or 2FA) for especially sensitive accounts.

- Avoid typing passwords while using public Wi-Fi. Instead, use a VPN or avoid websites that require your login information.

Financial advisory firms have historically endured a bad reputation – either because they were too expensive, or they only helped people with lots of money to invest, or they were trying to sell clients a product or plan that didn’t align with the heart of their goals and situation. Too many Americans don’t think they can afford a Financial Advisor and planning services. Too many of them avoid partnering with an Advisor because they don’t think they have enough money to meet some criteria. But those are often the people who could benefit from a financial coach the most! It’s also the largest population in America. That’s why we founded Trilogy Financial almost 30 years ago – to provide a true fiduciary and financial coach to everyday Americans who want to live the best life possible. Our goal at Trilogy was to create something different, something people hadn’t seen before. And over the last 25 years, we’ve been evolving the firm and honing our practices to improve the financial planning industry and make an Advisor accessible to everyone.

A Purpose Driven Financial Advisor and Coach

In Trilogy Financial’s beginnings, our vision and purpose was to help Financial Advisors be better Advisors so they could help more people. However, as time has gone on, that’s evolved into something bigger. Now our purpose is to help everyday Americans gain financial independence. They are the group of people that often struggle to achieve their financial goals, and we want to focus and help those that need advice. This is the culture we’ve built today. Our Advisors want to help as many people as they can, and we’re on a mission to make those Advisors more productive so that can help provide more for our clients. That is purpose-driven business.

How to Make Financial Advisors More Productive For Clients

Most financial advisory and planning firms have an advisor-led service model, and there’s nothing wrong with that – except that not all Advisors have service as their strong suit. As a Financial Advisor, many people perceive our job is to advise people how to save and spend their money. But we believe it takes more than that to make an impact. We’re striving to build what we call a “trust transfer” where our Advisors spend more time advising clients, building Life Plans, and making recommendations, and a service team does what they do best. This is how we’re optimizing our operations at Trilogy for the benefit of our clients. This service team consists of a group of people with a distinct culture and skillset that will deliver great, helpful service to our clients. This is contrary to what’s “the norm” for financial advisory firms – and that’s exactly why we’re doing it. This is part of our efforts to bring quality financial planning and advice to everyday Americans.

Introducing the Mack Service Center

The Mack Service Center is a robust client experience service center that was Trilogy’s late co-founder Kevin “Mack” Mackintosh’s vision for the firm. His core focus was to build a meaningful client service team to support Advisors so they could do what they do best – financial planning – and provide the clients with a high quality experience. Mack designed and developed the Trilogy Service Team based on what he learned over the years as an Eagle Scout, rowing crew member and in his time in the financial planning business. From day one, he had a clear vision of what Trilogy could accomplish when we all worked together and focused on service. A few years back, he took the ball and really got it rolling for this project. He found the right people to lead it and get it off the ground. Right before his untimely passing in early 2020, he had nearly completed building the Service Center team vision. Following his loss, under the leadership of our founder/President, Jeff Motske, in conjunction with Eric Perkins – we built out the actual Service Center, team, outlined processes, operations and more. Kevin Mackintosh instilled the right attitude, built the right culture and we’re proud to name our Mack Service Center after him so his legacy lives on.

The Future of Trilogy Financial and the Mack Service Center

Our goal is to have a well-regarded Advisor in front of every everyday American. Too many financial advisory firms want to work with high-net-worth individuals, but it’s those who are 52 years old with $400,000 in their retirement who really need our support and education to get to where they want and need to be. These are everyday Americans, and they deserve for someone to help them pursue their dreams. And we’re changing that. We rolled out the Mack Service Center team this year to support our Financial Advisors’ current planning efforts with each client. This is our way of connecting the financial planning industry back with the real-life issues of Americans and helping each of them plan and live the life of their dreams.

![]()

The recently implemented SECURE Act can be confusing to understand. With my free eBook and customized advisory services, I can help you navigate how the SECURE Act may impact your financial strategy moving forward. Curious about what it means for you? Download the eBook for an overview of the SECURE Act. We're here to help.

Download the eBook here

As you approach retirement it's important to explore your options, health-care concerns, and get the best advice to successfully transition into those golden years. Learn how to prepare for retirement and navigate your Social Security benefits. We're here to help.

Download your free eBook to learn more